How to Find Out If Your House Is in a Flood Zone

Three ways to check whether your property is in Flood Zone 2 or 3, what the flood zones mean, and how it affects insurance, mortgages and planning.

Checking a specific address?

Skip the theory — put the address in and see every constraint recorded against it, free.

Postcode, address, grid reference or UPRN. England, Wales and Scotland, free, no signup.

Flooding is one of the biggest risks to property in England. If your house is in Flood Zone 2 or 3, it can affect your insurance premiums, mortgage options, and what you're allowed to build. Here's how to check — and what to do about it.

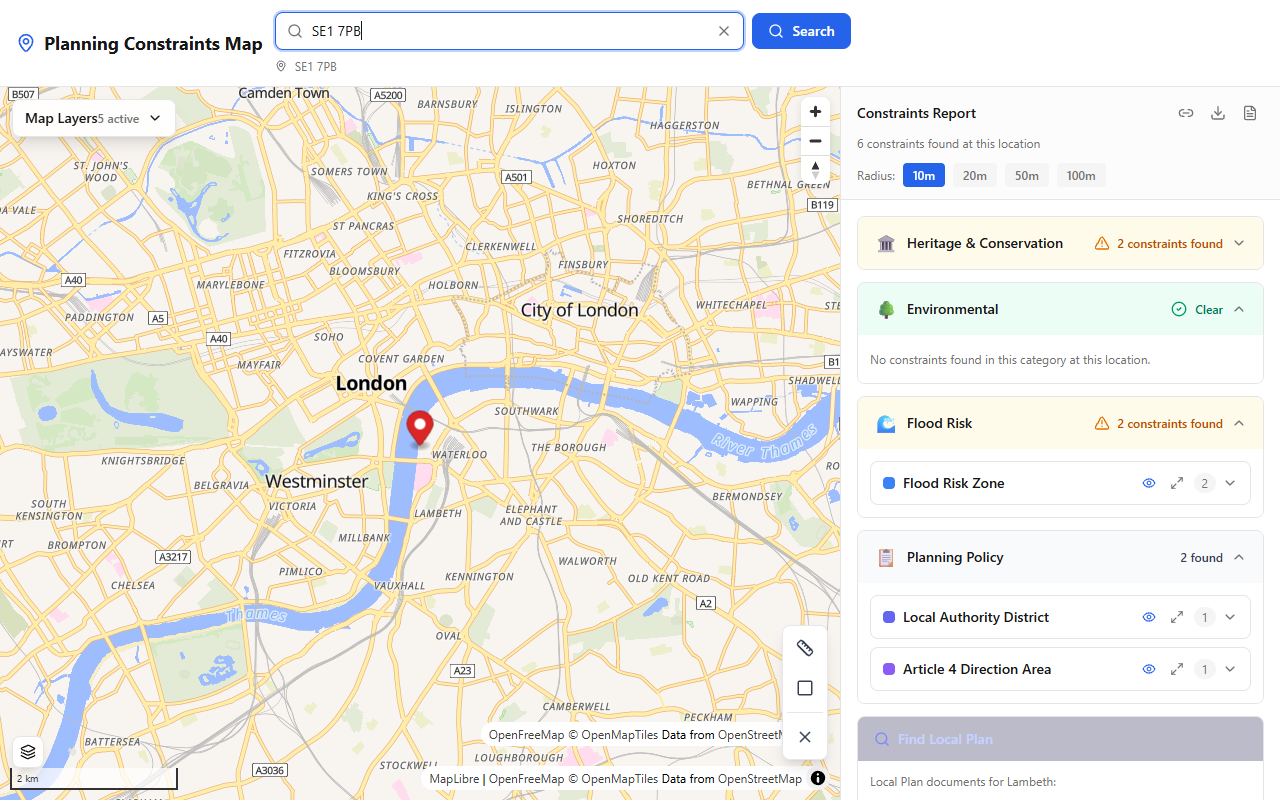

Method 1: Use our free planning constraints tool

The Planning Constraints Map shows Flood Zone 2 and Flood Zone 3 boundaries from Environment Agency data, alongside every other planning constraint.

Flood Risk Zone results shown in the constraints panel, with heritage and planning policy categories also visible.

- Open the Planning Constraints Map

- Search for your postcode or address

- Check the results panel for flood zone entries

- The flood zone boundaries appear on the map in blue shading

You'll see immediately whether your property falls within Flood Zone 2 (medium probability) or Flood Zone 3 (high probability). If neither appears, you're in Flood Zone 1 (low probability).

Method 2: Environment Agency flood map

The Environment Agency maintains the official Flood Map for Planning. Enter your postcode and it shows Flood Zone 2 and 3 boundaries. This is the same dataset our tool uses, presented on the EA's own mapping.

For a broader picture that includes surface water flood risk (which is separate from river/sea flood zones), use the Check your long-term flood risk service. This shows risk from rivers, the sea, surface water, and reservoirs on a single page.

Method 3: Property search or insurance quote

During a property purchase, the Local Authority Search and environmental searches will identify flood risk. Your solicitor may also commission a specific flood risk report from a provider like Groundsure or Landmark.

Another informal way to gauge flood risk is to get insurance quotes. If flood cover is expensive or difficult to obtain, that's a strong signal that the property is in a higher-risk area.

What do the flood zones mean?

The Environment Agency classifies land into three zones based on the probability of flooding from rivers and the sea. These ignore flood defences — they show the underlying risk.

Flood Zone 1 — Low probability

Less than 0.1% (1 in 1,000) chance of flooding in any year. Most of England is in Flood Zone 1. There are very few planning restrictions related to flooding.

Flood Zone 2 — Medium probability

Between 0.1% and 1% chance of river flooding, or between 0.1% and 0.5% chance of sea flooding in any year. You'll need a Flood Risk Assessment for any development, and the council may apply the Sequential Test (checking whether the development could go somewhere at lower risk instead).

Flood Zone 3 — High probability

1% or greater chance of river flooding, or 0.5% or greater chance of sea flooding in any year. Development faces strict requirements including both the Sequential Test and potentially the Exception Test. Some areas within Flood Zone 3 are classed as "functional floodplain" where only water-compatible development is normally permitted.

How flood zones affect you as a homeowner

Insurance

Properties in Flood Zone 3 often face higher premiums. The Flood Re scheme caps flood insurance costs for eligible residential properties, but it only covers homes built before 1 January 2009. Newer properties in high-risk areas may struggle to get affordable cover.

Mortgages

Some lenders are cautious about properties in Flood Zone 3 and may require evidence of insurance before approving a mortgage. In extreme cases, lending may be declined.

Extensions and building work

If you want to extend or alter a property in a flood zone, you may need to include flood mitigation measures:

- Raising finished floor levels above predicted flood level

- Using flood-resilient materials (e.g., tiled floors rather than carpet, waterproof plaster)

- Installing flood barriers on doors and airbricks

- Placing electrical sockets above the predicted flood level

Property value

Research suggests properties in areas that have experienced flooding can see values reduced by 5–15%. However, the impact varies greatly depending on circumstances — a property with good defences and insurance may be less affected.

Don't forget surface water

Flood zones only cover river and sea flooding. Surface water flooding — caused by heavy rainfall overwhelming drains — is a separate risk. Some properties in Flood Zone 1 have significant surface water flood risk.

Check the Environment Agency's long-term flood risk service for a complete picture including surface water risk.

Summary

Three ways to check your flood zone:

- Quickest — Use the Planning Constraints Map for instant results

- Official source — Use the Environment Agency flood map

- During purchase — Environmental searches through your solicitor

If you're in Flood Zone 2 or 3, it doesn't mean you can't live there or make improvements — but you need to factor flood risk into your plans, insurance, and any building work.

Survey your own site — free

See every planning constraint at any address in England, Wales or Scotland in seconds: conservation areas, listed buildings, flood risk, Article 4 and 140+ more. Need it on paper? The Full Survey Report with plain-English guidance is £9.99.